Delta and Theta Explained: The Two Greeks That Matter Most When You Start

Delta and Theta Explained: The Two Greeks That Matter Most When You Start

Part 3A of 10 in the Options for FIRE Investors series

A quick note on structure before we start: when I planned this series, Part 3 was going to be "the Greeks" — Delta, Gamma, Theta, and Vega, all in one post. I changed my mind while writing it. Four new, interacting concepts in one sitting is exactly how beginners end up nodding along without actually absorbing any of it. So this is now a two-parter: 3A covers Delta and Theta — the two Greeks that matter most day-to-day, especially once we get into premium-selling strategies later in this series. 3B, coming next, covers Gamma and Vega — the two "risk" Greeks that matter most when volatility moves or expiration gets close. Same total ground, just given room to actually land.

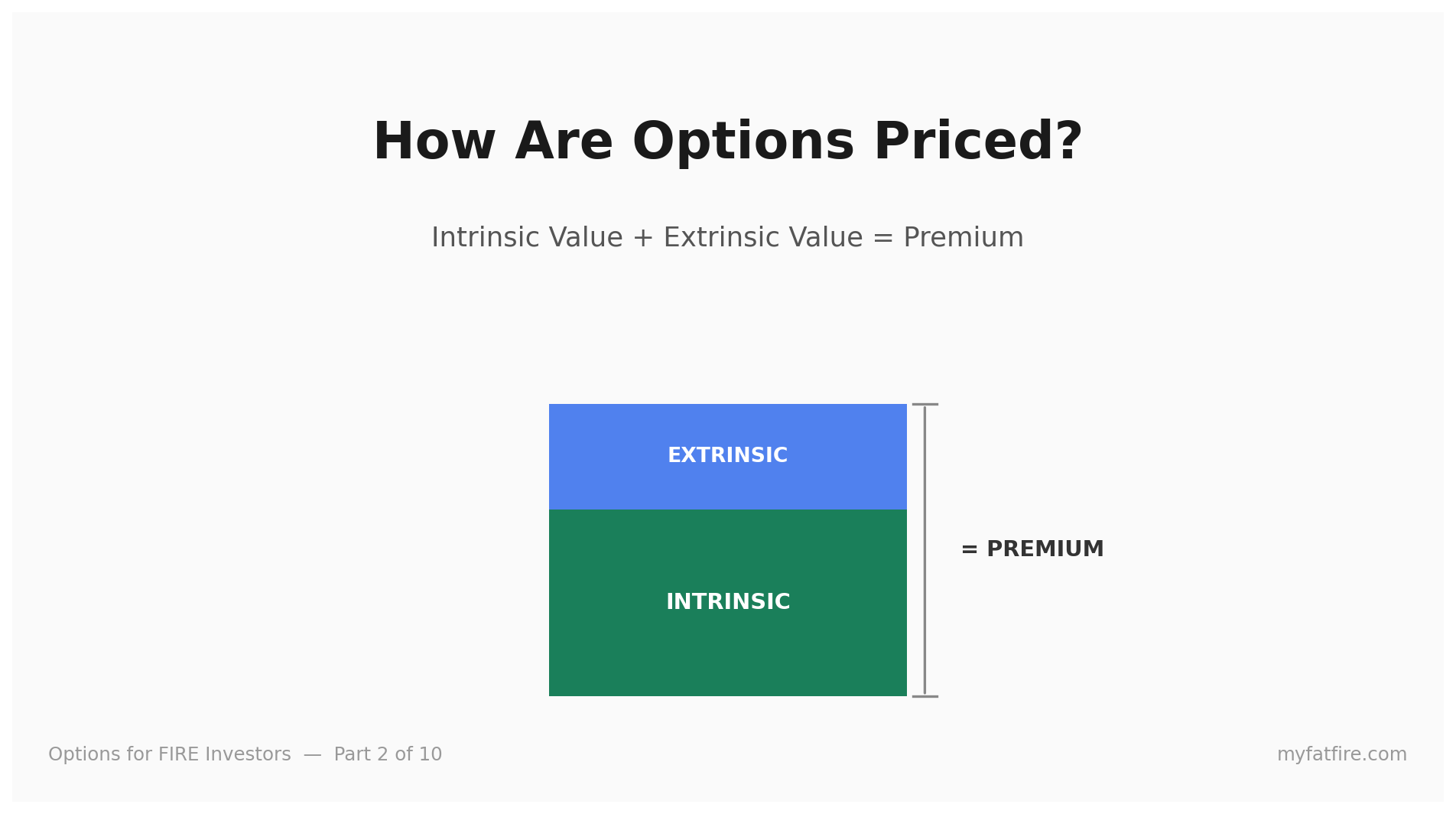

In Part 2, we split an option's premium into intrinsic and extrinsic value, and watched that extrinsic value quietly shrink over time even while the stock sat still. That shrinking has a name. And the way an option's price moves when the stock moves also has a name. Those two names are Delta and Theta, and once you can read them, an option chain stops being a wall of numbers and starts being a dashboard.

What "The Greeks" Actually Are

The Greeks are a set of numbers, recalculated constantly, that each measure how sensitive an option's price is to one specific thing changing — the stock price, the passage of time, volatility, and so on. You don't need to calculate them by hand. Every broker shows them to you directly on the option chain. Your job is just to know what each one is telling you.

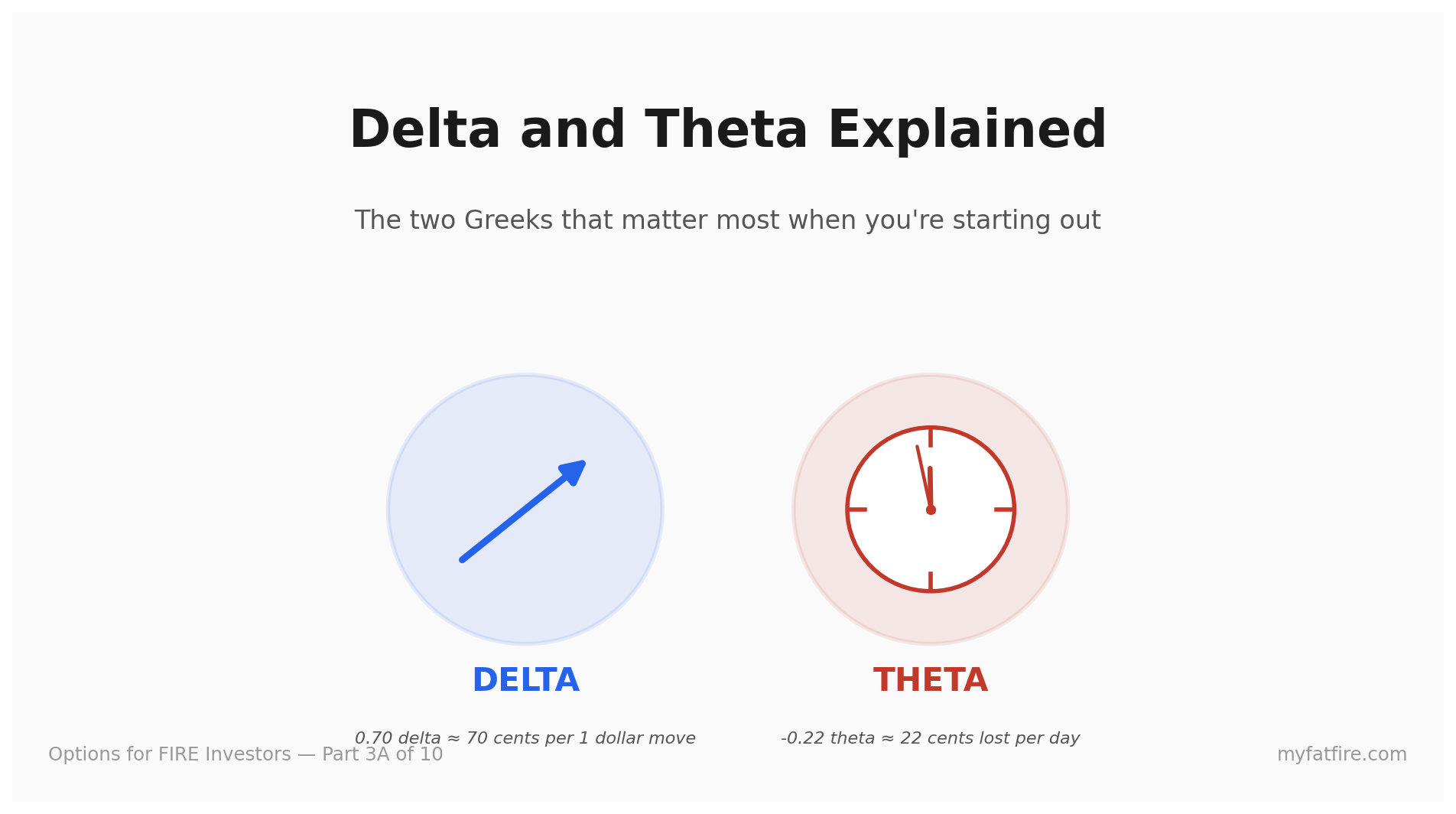

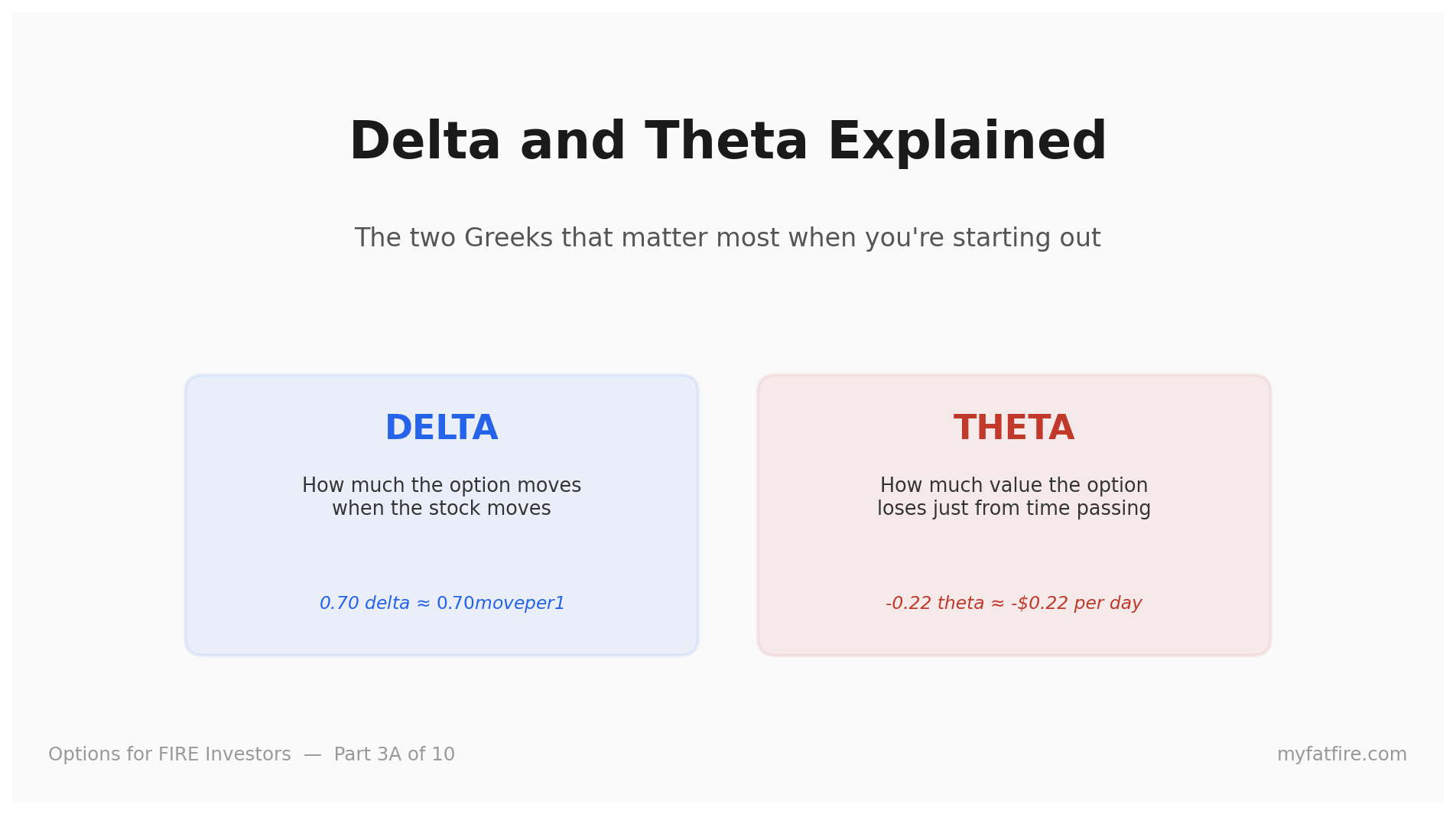

Today: the two that answer "how much does this move when the stock moves" (Delta) and "how much does this lose just from time passing" (Theta).

Delta: How Much Your Option Moves When the Stock Moves

Delta tells you, for every $1 move in the underlying stock, roughly how much the option's price will move.

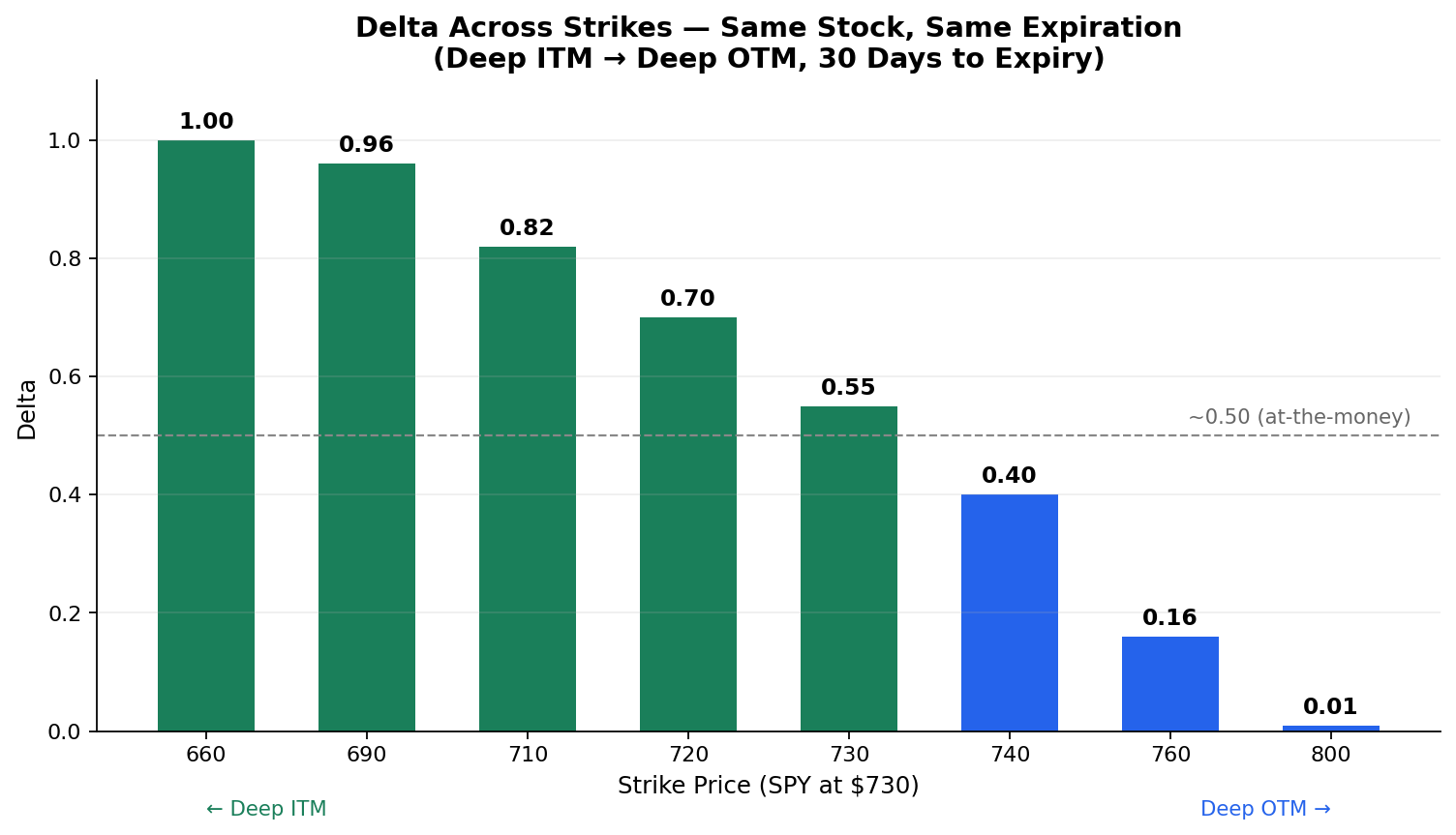

A call option with a delta of 0.50 will gain roughly $0.50 for every $1 the stock rises (and lose roughly $0.50 for every $1 it falls). A call with a delta of 0.20 barely budges when the stock moves — it's further out of the money, less sensitive. A call with a delta of 0.90 moves almost dollar-for-dollar with the stock — it's deep in the money, behaving almost like owning the stock outright.

Puts work the same way but with negative delta, since puts gain value when the stock falls.

Delta ranges from 0 to 1.00 for calls (0 to -1.00 for puts), and it isn't fixed — it shifts constantly as the stock price moves and as expiration approaches. As a rough anchor: an at-the-money option's delta sits near 0.50 (not exactly 0.50 — the precise value depends on volatility and time to expiration, but 0.50 is the right mental model for "the coin-flip point"). Move further in the money, delta climbs toward 1.00. Move further out of the money, delta drops toward 0.

There's a second, very practical way people use delta: as a rough stand-in for the probability the option expires in the money. A 0.30 delta option is often read as "roughly a 30% chance of expiring in the money." This is an approximation, not an exact probability — the true risk-neutral probability is a related but slightly different number — but it's close enough to be genuinely useful when you're sizing a trade or comparing strikes.

Why Delta Matters for Position Sizing

Here's the part that connects directly to your portfolio, not just the option chain: delta tells you your effective stock exposure.

One equity option contract represents 100 shares. If you own a call with a 0.50 delta, you have roughly the same directional exposure as owning 50 shares of the stock outright (0.50 × 100). Own two of those contracts, and you're exposed like 100 shares. This is why professional traders talk about "delta exposure" across an entire portfolio — it's the common currency that lets you compare a stock position, an option position, and a futures position on the same scale.

Theta: The Cost of Time

We already met this concept in Part 2 without naming it — the extrinsic value that quietly shrank even while SPY sat still. Theta is the number that measures exactly how much of that value disappears per day.

A theta of -0.05 means the option loses roughly $0.05 in value per day, all else being equal, purely from one day passing on the calendar. Nothing about the stock needs to move for this to happen. It happens on weekends. It happens on holidays when markets are closed. Time only moves in one direction, so theta is always working against an option buyer.

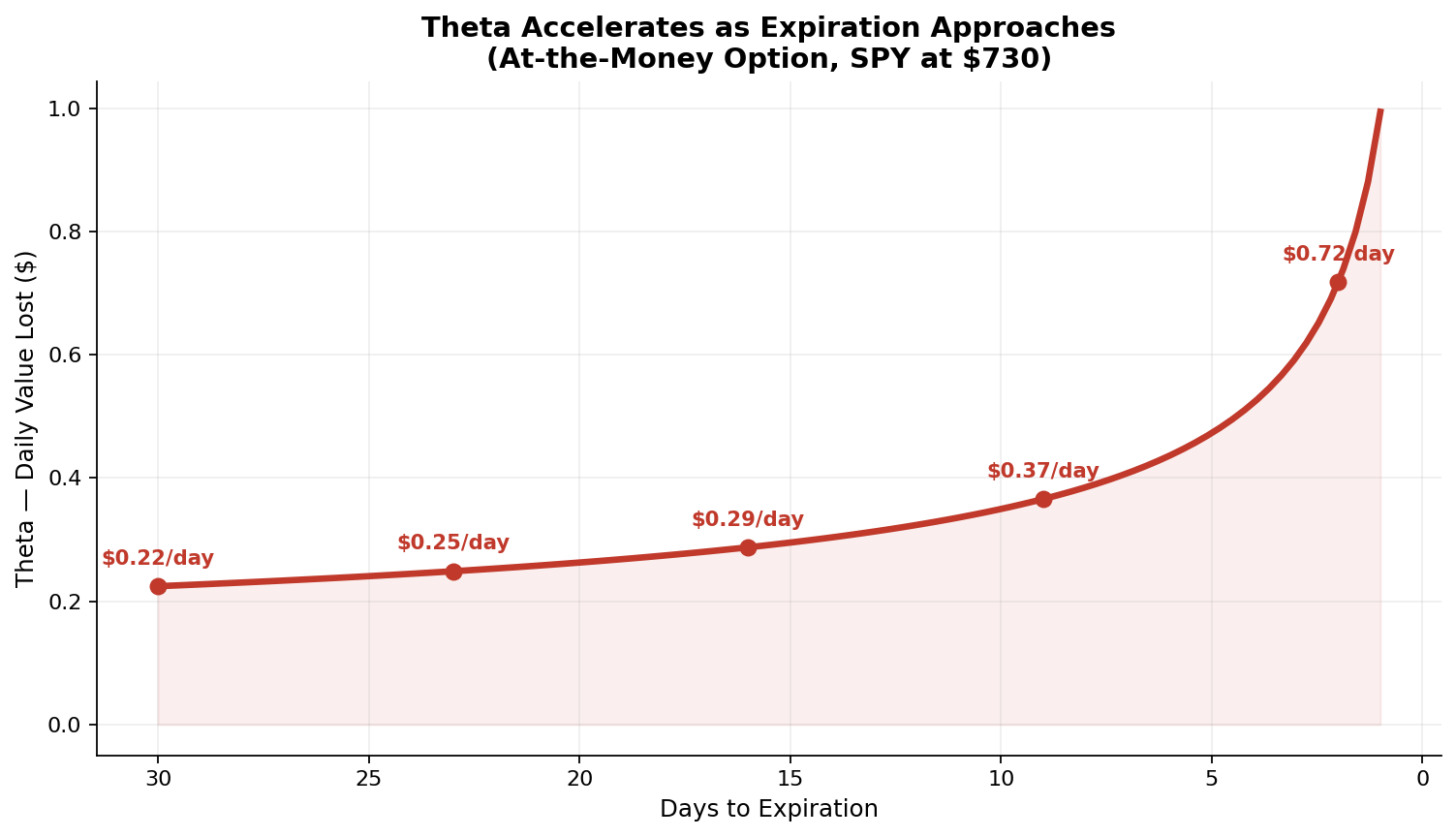

The part that surprises people: theta isn't constant — for an at-the-money option, it accelerates as expiration approaches. An at-the-money option with 30 days left decays slowly, maybe a quarter of a dollar a day. The same option with 2 days left can decay several times faster, even though nothing about the stock has changed. This is why the last week of an at-the-money option's life often feels like value is evaporating in front of you — because it genuinely is. (Worth noting: this acceleration pattern is cleanest for at-the-money options specifically — options that are deep in or out of the money can behave differently as expiration nears, which is a nuance for a later post.)

Why Theta Cuts Both Ways

Everything above sounds like bad news, but only if you're the option buyer. If you're the seller — the one who collected the premium in Part 1's insurance analogy — theta is working for you. Every day that passes without the stock making a big move is a day you keep more of what you collected. This is the entire logic behind premium-selling strategies: structure a trade so time decay is your income, not your enemy.

I'm not going to pretend that's a simple idea to execute well — sizing, strike selection, and risk management around it is most of what this series builds toward. But the core asymmetry is worth sitting with now: as a buyer, time is the enemy. As a seller, time is the ally. Nothing else in options trading matters more than internalizing which side of that you're on for any given trade.

Putting Both Together: The SPY Example, Continued

Back in Part 2, we looked at a SPY call, $720 strike, SPY at $730, with 30 days to expiration, priced at $18 ($10 intrinsic + $8 extrinsic).

That same option would show a delta of around 0.70 on your broker's screen (it's meaningfully in the money, so delta sits well above 0.50) and a theta of around -0.22 (losing roughly $0.22 a day at this point in its life).

Put plainly: if SPY rises $1 tomorrow, this option gains roughly $0.70 from delta — but also loses roughly $0.22 from theta, just from one day passing. Net, the option gains around $0.48. If SPY falls $1 instead, the option loses roughly $0.70 from delta and another $0.22 from theta — a rough total loss of $0.92. Notice the asymmetry: theta is a headwind either way, working against you whether the stock helps or hurts. If SPY doesn't move at all, the option simply loses the $0.22, pure decay, no stock movement required. This is the daily arithmetic every option position is quietly running, whether you're watching it or not.

A quick honest note on precision: these numbers come from a standard options-pricing model (Black-Scholes) using a realistic implied volatility for SPY. Your actual broker will show slightly different figures depending on the exact model it uses and real-time market conditions — but the magnitudes and the logic are accurate.

What's Coming Next in This Series

What is an option?

How options are priced — premium, intrinsic and extrinsic value 3A. Delta and Theta explained (this post) 3B. Gamma and Vega — the two risk Greeks

Calls and puts — buying vs selling, and why selling is different

Defined-risk strategies: spreads, why and how

Iron condors and butterflies explained

0DTE options — what same-day expiry actually means

Index options vs equity options — practical trading differences

Risk management — position sizing, delta exposure, drawdowns

Building a systematic options framework (a peek at how I actually trade)

Next up in 3B: what happens to delta itself when the stock moves fast (gamma), and what happens to every option's price when the market gets nervous, even if the stock doesn't move at all (vega). Those two show up constantly in anything involving 0DTE trading, so they're worth understanding properly before we get there.

One for the comments: does thinking about delta as "effective shares" change how you'd think about position sizing? And is there a specific number on your own option chain right now that you're not sure how to read? Tell me below — it'll shape where 3B goes deeper.