How Are Options Priced? Intrinsic vs Extrinsic Value explained

How Are Options Priced? Intrinsic vs Extrinsic Value Explained

Part 2 of 10 in the Options for FIRE Investors series

In Part 1, we covered what an option actually is — a contract giving you the right, not the obligation, to buy or sell something at a fixed price by a fixed date. I used the fire-insurance analogy: you pay a premium, and that premium buys you a right the seller is obligated to honor.

This week, the obvious next question: how is that premium actually calculated? Why does one option cost $2 and another, on the exact same stock, cost $40? The answer comes down to two components that every option's price is built from. Understand this split, and option chains stop looking like a wall of random numbers.

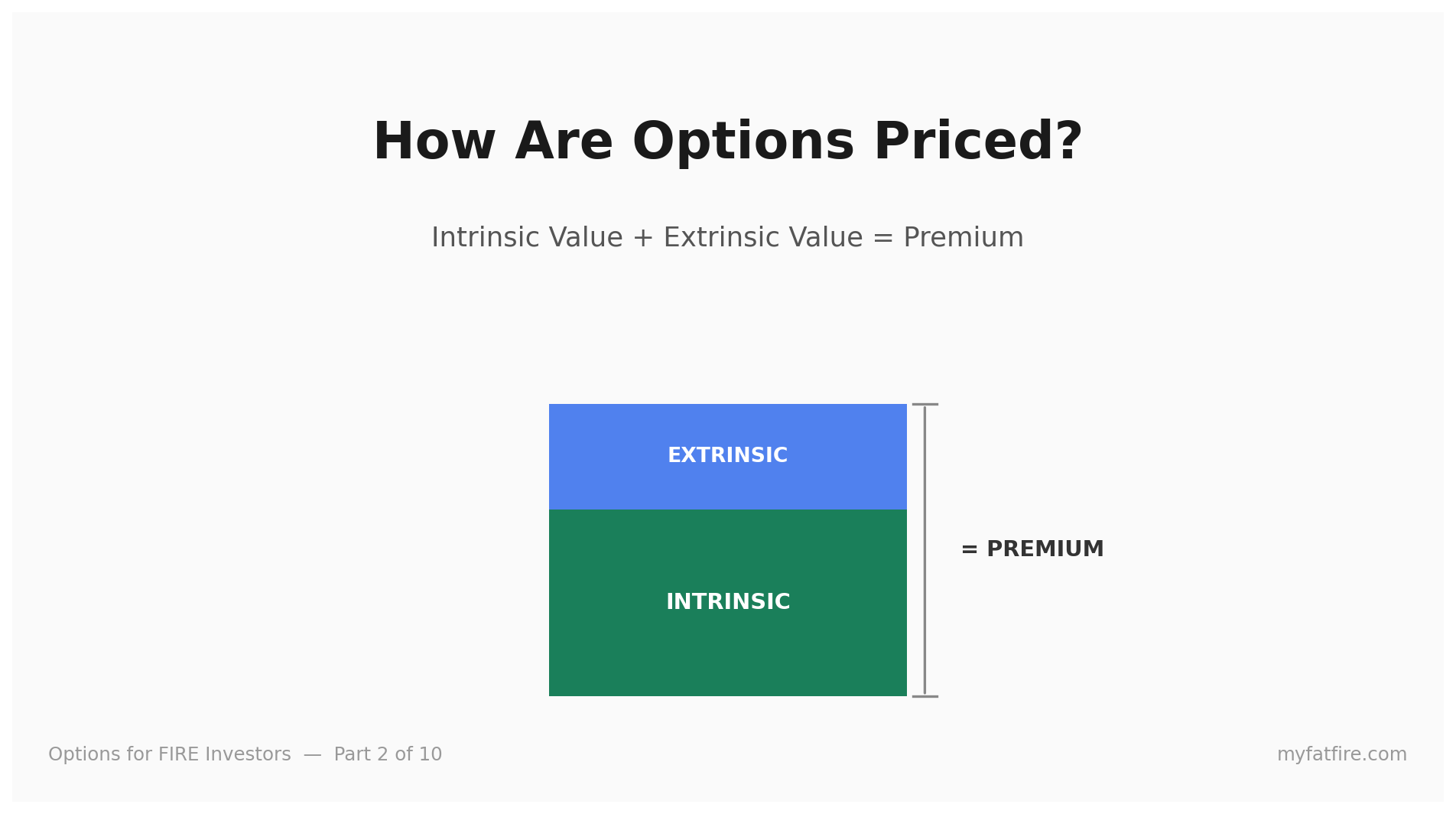

Premium = Intrinsic Value + Extrinsic Value

Every option's price, at any moment, breaks into exactly two pieces:

Intrinsic value — the value the option would have if you exercised it right now. This is pure math, no opinions involved.

Extrinsic value — everything else. The market's price for time, uncertainty, and possibility. This is the part beginners find confusing, because there's no single formula you can eyeball — it's a reflection of how much could still happen before expiration.

Add them together, and you get the premium — the price you actually see quoted on your broker's screen.

Intrinsic Value: The Easy Half

Intrinsic value only exists when an option is in the money — meaning exercising it right now would actually be worth something.

For a call option: intrinsic value = stock price − strike price (if positive; otherwise zero). For a put option: intrinsic value = strike price − stock price (if positive; otherwise zero).

That's the whole formula. No models, no assumptions.

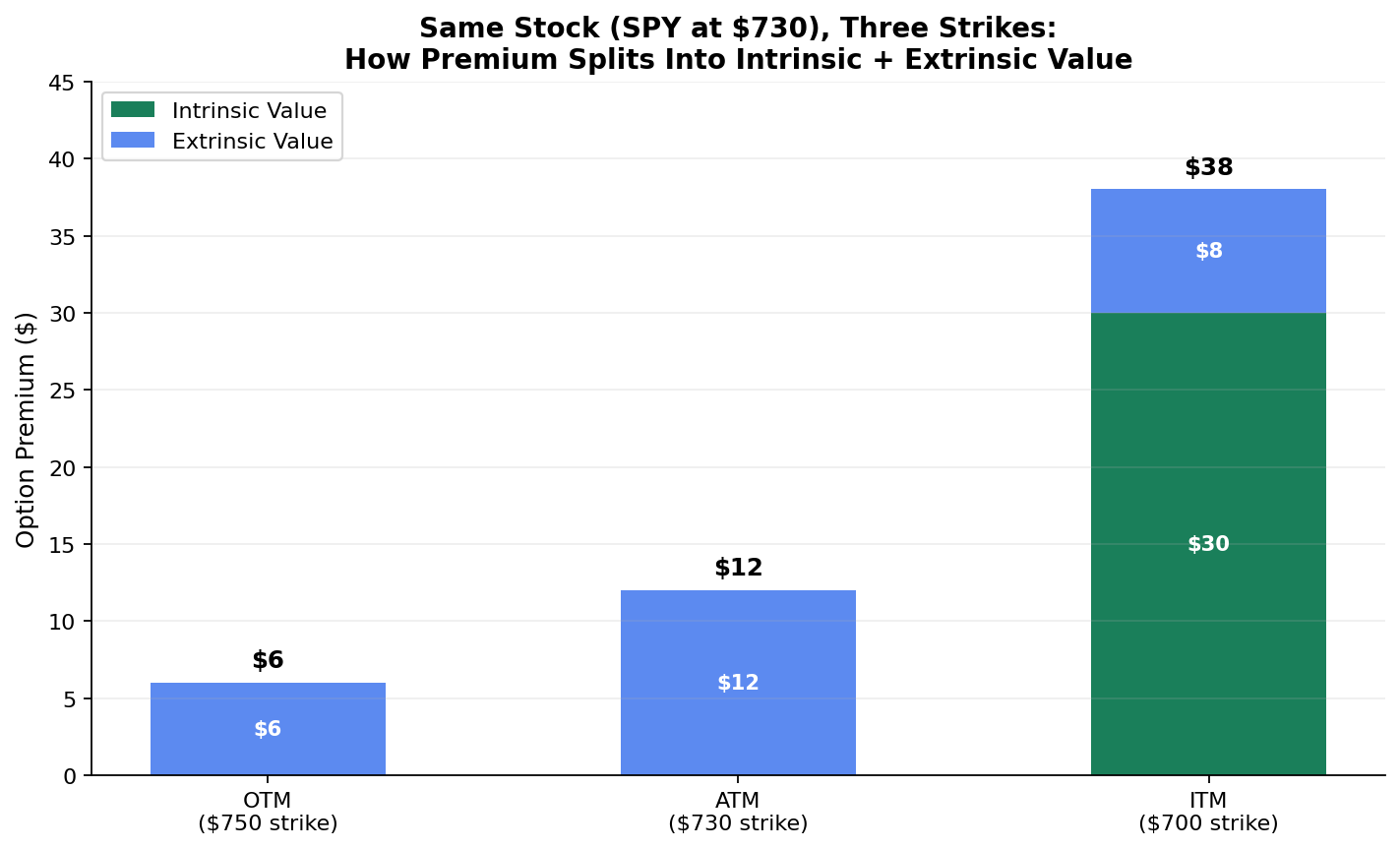

Take SPY, currently trading around $730. A SPY call option with a $700 strike has $30 of intrinsic value ($730 − $700), because if you exercised it this second, you'd be buying shares $30 below market price. A SPY call with a $750 strike has zero intrinsic value — exercising it would mean buying shares above the current market price, which nobody would do. That option is out of the money, and its entire premium is extrinsic value.

This gives us three states every option lives in:

In the money (ITM) — has intrinsic value. The call/put strike is favorable versus the current price.

At the money (ATM) — strike price is essentially equal to the current price. Intrinsic value is at or near zero.

Out of the money (OTM) — no intrinsic value at all. The entire premium is extrinsic.

Extrinsic Value: The Part Everyone Misreads

Here's where people go wrong: they assume an option with zero intrinsic value is "worthless." It isn't — it can still trade for real money, sometimes a lot of it, purely on extrinsic value.

Extrinsic value is driven by two forces:

1. Time remaining until expiration. The more time left, the more could happen — the stock has more room to move in your favor before the contract expires. An option expiring in 90 days has more time value baked in than the identical strike expiring tomorrow, all else equal. This is intuitive once you say it out loud: more time = more chances for the bet to work out, so the market charges more for it.

2. Implied volatility — the market's expectation of how much the stock might move. A stock everyone expects to sit still (think a slow-moving utility company with a 90-day option) will have cheap extrinsic value on its options. A stock with an earnings announcement landing before that same expiration — where a 10% overnight gap is genuinely on the table — will have expensive extrinsic value on the exact same strike, same days-to-expiration, same distance from the current price. The option isn't pricing in a direction. It's pricing in uncertainty.

This is why two options on different stocks, with the same days-to-expiration and the same distance from the current price, can trade at wildly different premiums. It's not noise — it's the market quantifying how unpredictable each stock is expected to be.

Why Premium Erodes Over Time

If you've ever bought an option, watched the stock do nothing, and noticed your option quietly lose value anyway — that's extrinsic value decaying. As each day passes, there's less time left for anything to happen, so the market pays less for that "possibility" component. This erosion has a name — theta — and it's significant enough that it gets its own dedicated post later in this series (Part 3, alongside the other Greeks). For now, the concept is what matters: extrinsic value melts away as expiration approaches, accelerating the closer you get to the final days. Intrinsic value, by contrast, doesn't erode at all — it only moves when the stock price moves.

This single fact is the foundation of an entire category of options strategies — including the short-premium, defined-risk structures I trade myself — because if you're the one selling the option rather than buying it, time decay works in your favor instead of against you. We'll get into that properly once we've covered the Greeks and the mechanics of selling options (Parts 3 and 4).

Reading This on an Actual Option Chain

Next time you pull up an option chain on your broker, you'll typically see a column for the bid/ask price — that's the premium, the full price you'd actually pay or receive. Intrinsic value usually isn't broken out as its own column, but you can calculate it yourself in seconds: take the stock's current price, compare it to the strike, and subtract. Whatever's left over after that subtraction is the extrinsic value — even though most platforms won't compute that for you on screen.

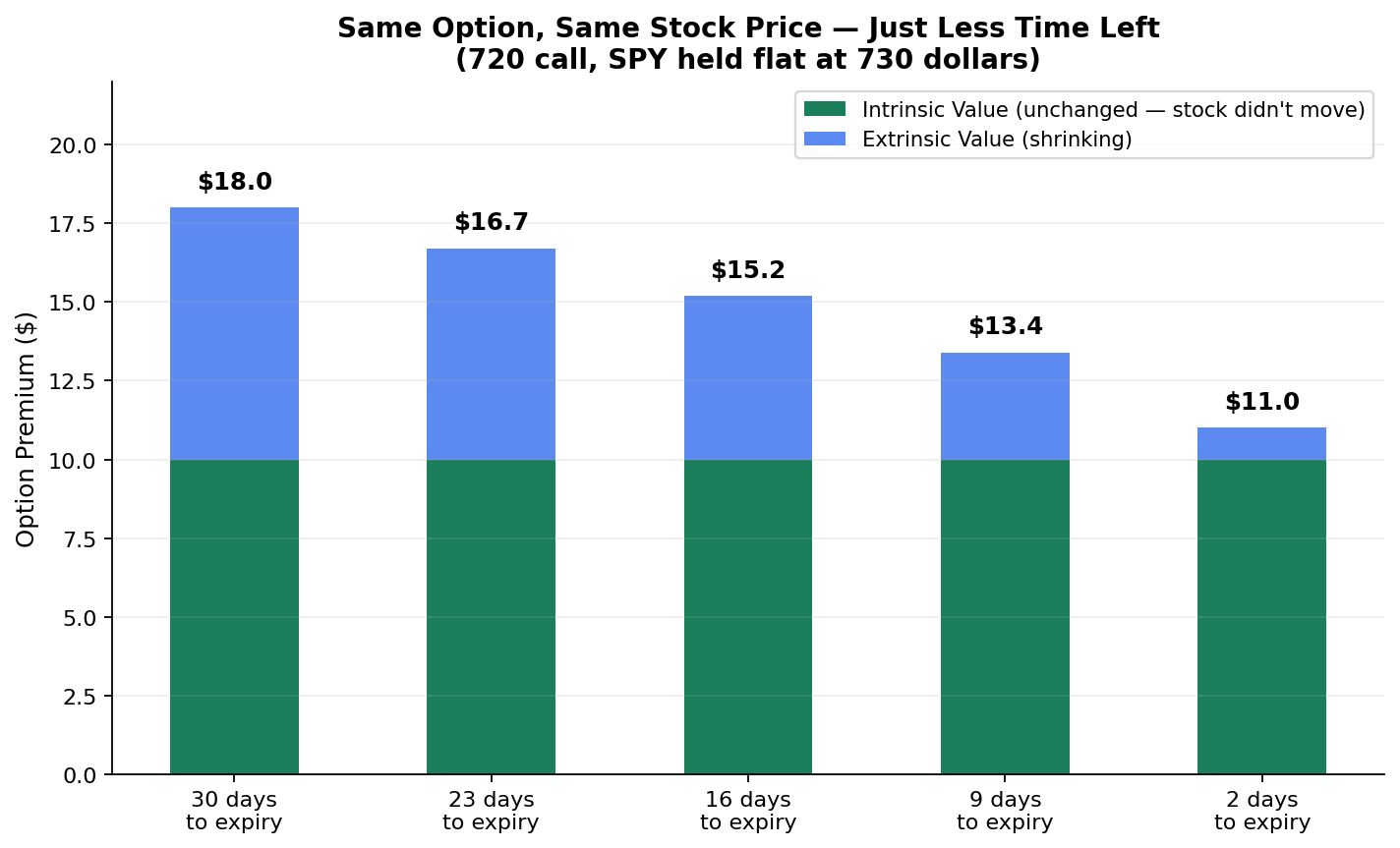

A quick worked example: say SPY is at $730, and you're looking at a call option with a $720 strike trading for $18.

Intrinsic value = $730 − $720 = $10

Extrinsic value = $18 (premium) − $10 (intrinsic) = $8

That $8 is the market's price for the time and uncertainty remaining on the contract — nothing more mystical than that.

The same logic flips for puts. Say you're looking at a SPY put with a $740 strike, also trading for $18, with SPY still at $730.

Intrinsic value = $740 − $730 = $10 (the put lets you sell at $740 when the market is only paying $730 — that $10 gap is real value)

Extrinsic value = $18 − $10 = $8

Same split, same logic, just mirrored — because a put's intrinsic value comes from the strike being above the stock price, while a call's comes from the strike being below it.

Now watch what happens to that $8 of extrinsic value as time passes, even if SPY doesn't move a single cent. Say that $720 call has 30 days left today. A week from now, with SPY still sitting at exactly $730, the option won't still be worth $18. The intrinsic value is unchanged — it's still $10, because that's pure math tied to the stock price. But the extrinsic value will have shrunk, maybe down to $6 or $5, simply because there's less time left for anything to happen. Nothing about the stock changed. The calendar did. That's the entire concept of time decay in a nutshell, and it's worth sitting with before we get to theta itself next week — because once you can see this $8 melting on its own, the formal version in Part 3 will feel like a formality, not a new idea.

What's Coming Next in This Series

What is an option?

How options are priced — premium, intrinsic and extrinsic value (this post)

The Greeks: Delta, Gamma, Theta, Vega explained simply

Calls and puts — buying vs selling, and why selling is different

Defined-risk strategies: spreads, why and how

Iron condors and butterflies explained

0DTE options — what same-day expiry actually means

Index options vs equity options — practical trading differences

Risk management — position sizing, delta exposure, drawdowns

Building a systematic options framework (a peek at how I actually trade)

Next week we'll open up the Greeks — the four numbers that actually drive everything we just talked about, including exactly how fast that extrinsic value erodes and how sensitive an option's price is to the stock moving.

Quick one for the comments: when you look at an option chain now, does the intrinsic/extrinsic split make the prices make more sense, or is there a specific part of this that's still murky? Tell me where you're stuck — it shapes what I dig into next.